Method for determining net present value npv. What is the NPV of a project. Making investment decisions based on the NPV criterion

Both concepts from the title of this section, discounted (present) value, PS (presentvalue, or PV), And net present value, NPV (netpresentvalue, or NPV), denote current the value of expected future cash receipts.

As an example, consider valuing an investment that promises an income of $100 per year at the end of this year and the next four years. We assume that this series of five payments of $100 each is guaranteed and the money will certainly arrive. If a bank were to pay us 10% annual interest on a five-year deposit, then that 10% would be the opportunity cost of the investment—the benchmark rate of return against which we would compare the benefits of our investment.

You can calculate the value of an investment by discounting its cash flows using opportunity cost as the discount rate.

Calculation formula inExceldiscounted (present) value (PV)= NPV(C1,B5:B9)

Present value(PS) in the amount of $379.08 is the current value of the investment.

Suppose this investment were to sell for $400. Obviously, it would not be worth the asking price, since - assuming an opportunity return (discount rate) of 10% - the real value of this investment would be only $379.08. it is appropriate to introduce the concept net present value(NPS). Denoted by the symbol r discount rate for this investment, we get the following NPV formula:

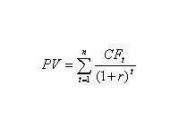

Where CF t is the cash flow from the investment at time t; CF 0 – flow of funds (receipt) at the current moment.

Calculation formula inExcel net present value (NPV)= NPV(C1,B6:B10)+B5

Excel terminology for discounted cash flows differs slightly from standard financial terminology. In Excel, the abbreviation MUR (NPV) denotes present value (not chiI'm standing present value) of a series of cash receipts.

To calculate in Excel net present value series of cash receipts in the usual sense of financial theory, you must first calculate present value future cash flows (using an Excel function such as NPV), and then subtract the initial cash flow from that number. (This value is often the same as the value of the asset in question.)

Not all investments involve the same risk. An office building project is riskier than investing in government securities, but probably carries less risk than investing in a start-up biotech. Let's say, according to your estimates, the project is associated with the same risk as investing in the stock market (investing in shares), and the return on the latter is projected at 12%. Then 12% is the appropriate value for the opportunity cost of raising capital. This is exactly the return that you give up by not investing in securities comparable in risk to your project. Now you can recalculate the NPV:

![]()

NPV = PV − $350,000 = $357,143 − $350,000 = $7,143

If other investors agree with your income forecast of $400 thousand. and with your assessment of the inherent risk, your property under construction should be worth $357,143. If you tried to sell it for more, you would not find a buyer, because then the expected return on investment in real estate would be lower than the 12% that can be obtained in the stock market. The office building still provides a net increase in value, but it is much less than our previous calculations indicate.

The value of an office building depends on the timing of cash flows and their inherent uncertainty. Income of 400 thousand dollars. would cost exactly 400 thousand dollars if it could be received immediately. If constructing an office building is as safe as investing in government securities, a delay of 1 year reduces the cost to $373,832. If it carries the same risk as investing in the stock market, uncertainty reduces the value by another $16,689, to $357,143.

Unfortunately, estimating the value of assets taking into account time and uncertainty is often much more difficult than our example suggests.

So, we came to the conclusion that the construction of an office building is a good thing because its value exceeds the costs associated with it, that is, it has a positive net present value. To calculate the cost, we estimated how much you would need to pay to get the same return on investing directly in the securities. The present value of the project is equal to the future revenue from it, discounted by the yield of these securities.

Another way to put the same point is that our real estate project makes sense because its return exceeds its cost of capital. Return on investment is simply the ratio of profit to initial cost:

Costs of capital (costs of raising capital), recall, are equal to the profitability lost due to refusal to invest in securities. If building the office building in our example involves the same risk as investing in the stock market, then there is a lost return of 12%. Since the 14% return on an office building exceeds the 12% opportunity cost, you should proceed with the project.

Here are two equivalent rules to follow when making investment decisions.

1. Net present value rule: make investments that have a positive net present value.

2. Rule of return: make investments whose profitability exceeds their opportunity costs.

The opportunity cost of raising capital is such an important concept that it deserves additional attention and another example. Let's say the following opportunity opens up before you: invest $100 thousand today, so that at the end of the year, depending on the general state of the economy, you will receive a return in the amount of:

You reject optimistic (rise) and pessimistic (decline) forecasts. This leaves you with an expected return of Q = $110,000. , that is, a 10% return on your investment (100 thousand dollars). But what is the correct discount rate?

You start looking for common stocks that have the same risk as your investment opportunity. Shares X turned out to be the most suitable. Their price for next year, in a normal state of the economy, is projected at $110. In case of an economic upswing, the price will be higher, in case of a downturn, the price will be lower, but the proportion of changes is the same as for your investment ($140 in an upturn, $80 in a downturn). In general, you conclude that stock X and your investment involve equal risk.

The current price of X stock is $95.65. per share, their expected return is 15%:

This is the same expected return that you give up by investing in your project instead of investing in the stock market. In other words, this is the opportunity cost of your project.

In order to estimate the cost of a project, you need to discount the expected cash flow at these opportunity costs:

![]()

This is exactly the amount it would cost investors in the stock market to purchase the expected cash flow of $110,000. (They could get it by buying 1,000 shares of X.) Therefore, that's exactly what investors will be willing to pay you for your project.

We get the net present value of the project by subtracting the initial investment:

NPV = $95,650 – $100,000 = −$4350

The project costs $4,350. less than what was spent on it. There's no point in taking it on.

Note that you would reach the same conclusion by comparing the project's expected return to its inherent cost of capital:

The project's expected return of 10% is less than the 15% that investors expect to earn by investing in the stock market, so, whatever one may say, the project is worthless.

Of course, in real life, the true state of the economy cannot be reduced to just “recession,” “normal,” or “boom.” In addition, we adopted another simplified premise, establishing an absolute correspondence between the return on 1000 shares of X and the proceeds from the investment project. However, the main idea of this example is quite consistent with real life. Remember: the opportunity cost of raising capital (cost of capital) for an investment project is equal to the expected return that investors require from common stock or other securities that are subject to the same risk as the project. By calculating the present value of a project, that is, by discounting its cash flow at opportunity costs, you get the amount that investors (including the shareholders of your own company) are willing to pay for the project. Whenever you find and launch a project with a positive net present value (that is, a project whose present value exceeds the investment required), you make your company's shareholders richer.

For example, this circumstance can be misleading. Imagine that a banker comes to you and says: “Your company is a well-established, reliable enterprise, and you have little debt. My bank is not averse to lending you the $100 thousand needed for the project at 8% per annum.” Does this mean that the cost of capital for the project is 8%? If so, your project is afloat: its present value at a rate of 8% is equal to $110,000/1.08 = $101,852, that is, the net present value is $101,852. — $100,000 = +1852 dollars

But this is not true. First, the interest rate on the loan has nothing to do with the risk of the project: it only reflects the health of your current business. Second, whether you take out a loan or not, you will still have to choose between a project with an expected return of only 10% and a stock that carries equivalent risk but has an expected return of 15%. A financial manager who borrows money at 8% and invests it at 10% is not just stupid, but desperately stupid, if the company or its shareholders have the opportunity to borrow money at 8% and invest with the same risk, but with profitability 15%. So it is the expected stock return of 15% that represents the opportunity cost of raising capital for the project.

Rationale for the net present value rule

So far, our knowledge of net present value has remained very superficial. The phrase “increasing value” as a company goal sounds quite reasonable. But the net present value rule is more than just a requirement of basic common sense. We need to understand what this rule is and why managers look to the bond and equity markets to determine the opportunity cost of raising capital.

In our previous example, only one person (you) invested 100% of the money in a new office building and received 100% of the return on it. But in a corporation, investments are made on behalf of and at the expense of thousands of shareholders with different appetites for risk and different preferences regarding the choice between today's and future income (and therefore consumption). What if a project that clearly has a positive net present value for Ms. Smith turns out to be a deep loss for Mr. Jones? Could it happen that the goal of maximizing the value of the company will be unacceptable to some of them?

The answer to both questions is the same: no. Both Smith and Jones will always be able to come to an agreement if they have unfettered access to the capital market. We will show this with another simple example.

Suppose you are able to foresee your future earnings in advance. Without the ability to save from current income or take out a loan against future income, you will be forced to postpone consumption until you receive it. And this is a very inconvenient thing, to say the least. If the bulk of the income that is due to you in your life falls in some more or less distant future, then the result may be that today you are in danger of hunger, and tomorrow (or sometime later) - excessive consumption. This is where the capital market comes in handy. Simply put, a capital market is a market in which people exchange current and future money among themselves. Thanks to him, you can eat normally now and in the future.

We will now show how a well-functioning capital market can help investors with different income schedules and consumption patterns come to a consensus about whether a particular investment project is worth undertaking. Let's imagine two investors with different tastes and aspirations. One of them is Ant, who prefers to save money for the future; the other is Dragonfly, who squanders all her income with extraordinary ease, not caring at all about the future. Now let's assume that they both have the same opportunity: to purchase a stake in a $350,000 office building project that will yield a guaranteed return of $400,000 at the end of the year. (i.e. the yield is about 14%). The interest rate is 7%. At this rate, both Ant and Dragonfly can borrow or lend money in the capital market.

No doubt Ant would be happy to invest in an office building. Every hundred dollars invested in this project today will allow him to spend $114 at the end of the year, while the same hundred invested in the capital market will bring him only $107.

What would Dragonfly, who wants to spend money right now, and not in a year, do? Perhaps she will neglect the investment opportunity and immediately squander all her cash? It’s unlikely, since the capital market allows you to both lend and borrow money. Every hundred dollars that Dragonfly invests in an office building will bring her $114 at the end of the year. Any bank, aware that Dragonfly will have a guaranteed income at the end of the year, will not hesitate to lend her $114/1.07 = $106.54 today. Therefore, if Dragonfly invests in an office building and then takes out a loan against future income, it will be able to spend not 100, but 106.54 dollars today.

The figure clearly illustrates this example (our heroes are designated here as M and C, respectively). The horizontal axis represents the amount of money that can be spent today; the vertical axis shows expenses for the coming year. Let's say that initially both the Ant and the Dragonfly have the same amounts - 100 dollars each. If each of them fully invests their $100. on the capital market, then at the end of the year both will receive $100 for expenses. x 1.07 = 107 dollars. The straight line connecting these two points (in the figure this is the line closest to the origin) displays combinations of current and future consumption for the following possible options: when nothing is invested, when this or that part of the cash is invested, and when all available funds are invested on the capital market at 7% per annum. (The interest rate determines the slope of this line.) Any intermediate point on the line (between the points of intersection with the coordinate axes) is reached when one or another part of the cash is $100. today is spent and the rest is invested in the capital market. Let's say someone might prefer to spend $50. today and $53.50. next year. But our Ant and Dragonfly unanimously rejected such intermediate (“residual”) consumption patterns.

The straight line with the arrow (highlighted) in the figure represents the proceeds from the investment of $100. in an office building construction project. The return on this investment is 14%, so today's $100. will turn into 114 dollars in a year.

The Dragonfly (C) wants to consume right now, while the Ant (M) wants to wait. But each of them is happy to invest. M prefers to invest not at 7, but at 14%, which increases the point of intersection of the straight line with the arrow (which is highlighted in blue) with the vertical axis. C also invests (at the same 14%), and then borrows money at 7%, thereby turning $100 intended for current consumption into $106.54. Thanks to his investment, C will have $114 in one year to pay off his debt. The net present value of this investment is $106.54. — 100 dollars. =+6.54 dollars

The inclined straight line on the right in the figure (the one that is located farthest from the origin) reflects the increase in the planned expenses of Ant and Dragonfly if they decide to invest their $100. to an office building. A tight-fisted Ant who does not intend to spend anything today can invest $100. in the construction of an office building and at the end of the year receive 114 dollars. for expenses. Lazy Dragonfly also invests $100. to an office building, but at the same time takes 114 dollars/1.07 = 106.54 dollars. for future income. It is clear that there is nothing stopping these spending plans. Indeed, the right straight line represents all possible combinations of current and future spending available to an investor who invests $100. in the construction of an office building and at the same time takes out a loan against some part of the future income.

From the figure it is easy to see that the present value of Dragonfly and Ant's participation in the office building project is $106.54, and the net present value is $6.54. (this is the difference between $106.54 present value and $100 initial investment). Despite the differences in tastes between Dragonfly and Ant, both of them benefit from investing in an office building and then using the power of the capital market to achieve the desired ratio between today's consumption and consumption at the end of the year. In fact, in making their investment decisions, both of them seem willing to follow two equivalent rules, which we formulated rather superficially at the end of the section. We can now rephrase them as follows.

1. Net Present Value Rule: Invest in any project with a positive net present value. The latter is the difference between the discounted, or present, value of future cash flow and the amount of the initial investment.

2. Rule of profitability: invest in any project whose profitability exceeds the profitability of equivalent investments in the capital market.

What would happen if the interest rate were not 7%, but 14.3%? In this case, the net present value of the office building would be zero:

![]()

In addition, the profitability of the project is $400,000/$350,000. - 1 = 0.143, or 14.3%, would be exactly equal to the capital market interest rate. In this case, both of our rules show that the project is balancing on the edge “between light and darkness,” and this means that investors should be indifferent whether the company takes it on or not.

As you can see, if the interest rate were 14.3%, neither the Dragonfly nor the Ant would gain anything from investing in an office building. Ant would have the same amount of money to spend at the end of the year regardless of how he initially used his money - investing it in an office building or investing it in the capital market. In the same way, Dragonfly would not receive any benefit by investing in an office building with a yield of 14.3% and at the same time taking out a loan at the same 14.3%. She might as well spend all her original cash at once.

In our example, Dragonfly and Ant invested the same funds in an office building construction project and willingly took part in it. This unanimity is explained by their equal opportunities to both borrow and lend money. Whenever a firm discounts cash flow at financial market rates, it is making the implicit assumption that its shareholders have free and equal access to competitive capital markets.

It is easy to see that the absence of a well-functioning capital market undermines the logic of our net present value rule. For example, let’s assume that Dragonfly does not have the opportunity to take out a loan against future income or that there is such an opportunity in principle, but the price of the loan is too high to take advantage of it. In such a situation, Dragonfly would likely prefer to use up his cash immediately rather than invest it in an office building and wait until the end of the year to start spending the money. If Dragonfly and Ant were shareholders of the same company, it would be difficult for the manager to reconcile their conflicting interests and goals.

No one would unequivocally assert that capital markets are characterized by perfect competition. Taxes, transaction costs, and other factors limiting perfect competition should be taken into account when making financial decisions. But by and large, capital markets operate quite efficiently. This is at least one good reason why net present value should be relied upon when setting corporate goals. Another reason is that the net present value rule simply agrees with common sense; Later we will see that it leads to obviously ridiculous results much less often than its main “competitors” - other common criteria for making investment decisions. For now, having only briefly touched on the problems of market imperfections, we, like a shipwrecked economist, will simply assume that we have a life jacket, and, mentally dressing ourselves up in it, we will calmly swim to the shore.

So far, our rationale for the net present value rule has been limited by two assumptions: that cash flows extend over only two time periods and that cash flows are inherently certain. However, the rule is also true for uncertain cash flows that continue into the distant future. The following arguments can be given to support this.

1. The financial manager must act in the interests of the owners of the company, that is, its shareholders. Every shareholder strives for three goals:

a) be as rich as possible, that is, maximize your real wealth;

b) convert this wealth into any temporary consumption model desired by him (or her);

c) have freedom in choosing the risk characteristics of this consumption model.

2. But shareholders do not need the help of a financial manager to achieve the best temporary consumption pattern. They can handle this themselves if they have easy access to competitive capital markets. In addition, they are free to choose the risk characteristics of their consumption patterns by investing in more or less risky securities.

3. How then can a financial manager help the company's shareholders? Only one way: by increasing the market value of each shareholder's share in the company. To do this, he must take advantage of any investment opportunity that has a positive net present value.

Shareholders, although they have different preferences, show remarkable unanimity regarding the amounts they are willing to invest in real assets. On this basis, they can unite into one company and entrust the management of affairs to professional managers without risk to themselves. Managers do not need to know anything about the tastes and preferences of shareholders and should not indoctrinate them with their own tastes and preferences. Their goal is to maximize net present value. Once they have succeeded, managers can sit back and rest with the confidence that they have done their best work in the best interests of their shareholders.

This implies a fundamental condition for the successful functioning of a modern capitalist economy. The separation of ownership from management is of great importance for most corporations, so delegation of management authority is essential. It's nice to know that all managers can be given one simple instruction: maximize net present value.

Sometimes you hear managers argue that their corporations have different goals. Thus, a manager might say that his job is to maximize profits. Well, that sounds pretty meaningful. After all, don't shareholders prefer a profitable company to an unprofitable one? However, it is unreasonable to proclaim pure profit maximization as a corporate goal. There are several reasons for this.

1. The task of “maximizing profit” immediately gives rise to the question: “What year’s profit?” Shareholders may not want the manager to boost next year's profits at the expense of later years' profits.

2. The company can increase future profits by reducing dividend payments and investing this money in investment projects. But given the low returns on such investments, this goes against the interests of shareholders.

3. Different accountants use different methods for calculating profits. You may find that a decision that improves profitability from one accountant's perspective makes it worse from another's perspective.

Principal corollary

We show that managers best serve shareholders' interests by investing in projects with positive net present value. But this brings us back to the principal-agent problem. How can shareholders (principals) make sure that managers (agents) are not solely pursuing their own interests? Shareholders cannot constantly monitor managers to see if they are shirking their responsibilities or maximizing the value of their own wealth. However, there are several organizational mechanisms that more or less ensure that the manager's heart is in the shareholders' pocket.

Members of a company's board of directors are elected by shareholders and are supposed to represent their interests. True, sometimes the board of directors is portrayed as a weak-willed extra, always siding with management. However, when a company's operations are in trouble and managers don't come up with a viable turnaround plan, the board of directors does its job. In recent years, companies such as Eastman Kodak, General Motors, Xerox, Lucent, Ford Motors, Sunbeam, and Lands End have seen senior executives resign from their positions as profitability declined and the need to revamp their business strategy became clear. .

Considering that the performance of the corporation leaves much to be desired, and the members of the board of directors are not energetic enough in calling managers to order, shareholders may try to change the board of directors at the next election. If this succeeds, the new board of directors will recruit a new management team. However, such attempts to re-elect the board of directors are quite expensive and thankless (rare of them are successful). Therefore, dissident shareholders usually do not engage in an unequal battle, but instead simply sell their shares.

However, the sale of shares itself carries a very powerful message. If enough holders dump a stock, the price of the stock goes down. This hurts the reputation of managers and their earnings. CEOs receive part of their compensation in the form of earnings-related bonuses or stock options, which pay well when stock prices rise but are worthless when stock prices fall below a certain threshold. In theory, this should encourage managers to increase profits and increase share prices.

Do managers protect the interests of shareholders?

If a company's leaders fail to maximize value, they are always exposed to the threat of a hostile takeover. The lower the price of a company's shares falls (as a result of inept management or due to incorrect policies), the easier it is for another company or group of investors to buy a controlling stake in its shares. In such a situation, the old management team will likely be left behind, and new managers will take their place, ready to make the changes needed to realize the true value of the company.

The mechanisms described go a long way toward ensuring that there are few executives at the top of large American corporations who are lazy or shareholder-neglected. Moreover, these mechanisms contain strong incentives for managers to work harder.

We conceptualized managers as agents working for the shareholders of their firms. But perhaps it is worth asking: “Is it desirable for managers to act in the selfish interests of shareholders?” Doesn't the focus on enriching shareholders mean that managers should behave like greedy traders, cruelly trampling on the weak and helpless? Don't they have a broader responsibility—to their employees, to their customers, to their suppliers, and to the community where the firm is located?

The bulk of this book is devoted to financial policies that increase firm value. None of these policies requires the disadvantage of the weak and helpless. In most cases, doing the right thing (maximizing value) is not at all inconsistent with doing the good thing. If a firm is profitable, then it is one whose customers are satisfied and whose employees are loyal; those firms whose customers and employees are dissatisfied with them are likely to experience declining profits and declining stock prices.

Of course, in business, as in any area of life, ethical issues arise; and when we call the firm's goal to maximize shareholder wealth, we do not mean that everything else should be left to chance. Laws partially prevent managers from engaging in obviously dishonest behavior, but for most managers it is not just the letter of the law or the provisions of formal employment contracts that are important. In business and finance, as in other everyday activities, there are unwritten and unspoken rules of behavior. In order to work fruitfully together, we must trust each other. The largest financial transactions are often “finalized” with a simple handshake, and each party knows that in the future, even if events turn out badly, the other party will not break its word. Any incident that weakens this mutual trust is detrimental to us all.

Should managers defend the interests of shareholders?

In many financial transactions, one party may be better informed than the other. It is very difficult to obtain complete and reliable information about the quality of the assets or services that you are purchasing. This situation opens up wide scope for dubious financial manipulations and illegal scams, and since unscrupulous businessmen are much more likely than honest entrepreneurs to jump from place to place, airport registration lists are replete with traces of financial scammers.

Honest firms counter this with a demonstrated commitment to long-term client relationships, a good name in the business and financial integrity. Large banks and investment companies are well aware that their most valuable asset is their business reputation. They never miss an opportunity to emphasize their long history of existence and their consistently responsible behavior. Any event that undermines this reputation can cause them enormous material damage.

Consider, for example, the Salomon Brothers stock exchange scandal that erupted in 1991. A company trader tried to circumvent the rules limiting its participation in a Treasury bond auction; To do this, he submitted bids on behalf of several Salomon Brothers clients without notifying them of this and without obtaining their consent. When the forgery was discovered, Salomon Brothers had to fork out a fair amount to settle the case: almost $200 million. went to pay the fine and another 100 million dollars. - to establish a special fund to satisfy claims in civil suits. In addition, the value of Salomon Brothers shares immediately decreased by more than $300 million. In fact, the shares fell in price by almost a third, reducing the company's market value by $1.5 billion.

What explains such a dramatic decline in the value of Salomon Brothers? Mainly due to the fears of investors, who felt that the company's business would suffer from the loss of customers who had lost confidence in it. The damage Salomon Brothers suffered as a result of its tarnished reputation was far greater than the obvious costs of the scandal, and hundreds or even thousands of times greater than the benefits that the company could have gained from illegal participation in the auction.

In this chapter we introduced the concept of present value as a tool for asset valuation. Calculating present value (PV) is simple. All you need to do is discount the future cash flow at an appropriate rate r, usually called the opportunity cost of capital, or marginal return:

Net present value (NPV) is equal to the sum of the present value and the original cash flow:

![]()

Recall that C 0 is negative if the initial cash flow represents an investment, that is, a cash outflow.

The discount rate is determined by the yield prevailing in the capital markets. If future cash flow is absolutely certain, the discount rate is equal to the interest rate on risk-free securities such as U.S. government debt. If the magnitude of future cash flow is subject to uncertainty, then the expected cash flow should be discounted by the expected return of securities with similar risk.

Cash flows should be discounted for two simple reasons: first, because a dollar today is worth more than a dollar tomorrow, and second, because a safe dollar is worth more than a risky one. The present value and net present value formulas express these ideas in numerical terms. The capital market is a market where the purchase and sale of reliable and risky future cash flows takes place. That's why we look at the rates of return prevailing in the capital markets to determine what discount rate to use given timing and cash flow risk. When we calculate the present value of an asset, we are actually estimating what people would pay for it given that alternative investment opportunities exist in the capital markets.

The concept of net present value supports the rationale for separating ownership from control within a corporation. A manager who invests only in assets with a positive net present value best serves the interests of each of the firm's owners—despite their differences in wealth and tastes. This is possible thanks to the capital market, which allows each shareholder to form their own investment portfolio in accordance with their needs. In particular, the firm does not need to adjust its investment policy so that subsequent cash flows correspond to shareholders' preferred temporary consumption patterns. Shareholders themselves are perfectly capable of moving funds forward or backward in time as long as they have free access to competitive capital markets. In fact, their choice of a particular temporary consumption pattern is limited by only two circumstances: their personal wealth (or lack thereof) and the interest rate at which they can borrow or lend money. The financial manager is not able to influence the interest rate, but he has the power to increase the wealth of shareholders. This can be done by investing in assets with a positive net present value.

There are several organizational mechanisms that provide some assurance that managers are paying close attention to the value of the firm:

- the work of managers is closely monitored by the board of directors;

- It is difficult for lazy people and hacks to hold on to their positions under the pressure of more energetic managers. Such competition often arises within an individual company, but it also operates externally: poorly performing firms very often become targets of hostile takeovers; as a result, as a rule, the management team is completely renewed;

- Managers are motivated by incentive schemes such as stock options, which pay handsomely when the stock price (and therefore shareholders' wealth) rises, but depreciate when it doesn't.

If managers strive to increase shareholder value, this does not mean that they are neglecting other, broader responsibilities to society. Managers act honestly and fairly towards employees, customers and suppliers partly because they see it as the common good, but partly for very pragmatic reasons: they are well aware that a company's most valuable asset is its reputation. Of course, there are ethical issues in finance, and every time some unscrupulous manager abuses his position, we all start to trust each other a little less.

The first works on net present value:

I. Fisher. The Theory of Interest. 1965 (reprint of 1930 edition). J. Hirshleifer. On the Theory of Optimal Investment Decision // Journal of Political Economy. 66: 329-352. 1958. August.

For a more detailed presentation of the subject, see:

E. F. Fama and M. H. Miller. The Theory of Finance. New York: Holt, Rinehart and Winston, 1972.

If you want to delve deeper into how managers can be more motivated to maximize shareholder wealth, we suggest looking at the following works:

M. C. Jensen and W. H. Meckling. Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure // Journal of Financial Economics. 3: 305-360. 1976. October.

E. F. Fama. Agency Problems and the Theory of the Firm // Journal of Political Economy. 88: 288-307. 1980. April.

However, needless to say, there are some types of real estate, the value of which is practically impossible for an appraiser to determine; for example, no one knows the potential price at which the Taj Mahal, or the Parthenon, or Windsor Castle could be sold.

Hereinafter, as symbols of terms in the text and in formulas, abbreviations derived from English names are used: PV - from present value (present value), NPV - from net present value (net present value), DF - from discount factor (coefficient discounting), D - from debt (debt), E - from equity (own, or share capital), etc. (A complete list of terms in Russian and English, as well as corresponding abbreviations (symbols) is contained in the Subject Index at the end of the book.) - Note. editor.

Let's check ourselves. If you invest $373,832. at 7% per annum, then at the end of the year your original investment will be returned to you plus interest income in the amount of 0.07 x $373,832. = $26,168 The total amount you will receive is $373,832. + $26,168 = $400,000 Pay attention to this: 373,832 x 1.07 = 400,000.

We'll define "expected" more precisely in Chapter 9. For now, it's enough to understand that expected revenue reflects a realistic forecast, not an optimistic or pessimistic forecast.

You can verify for yourself the equivalence of these rules. Let's express them differently: if the yield of 50,000/350,000 is greater than r, then the net present value of -350,000 + 400,000/(1+r) must be greater than zero.

These rules may conflict with each other when cash flows extend beyond two periods. We'll tackle this problem in Chapter 5.

We assume that a decline and a rise are equally probable, that is, that the expected (average) outcome is $110 thousand. Let, for example, the probabilities of recession, normal state and rise - that is, each of these probabilities - be equal to Y3. Then the expected return is: Q = ($80,000 + $110,000 + + $140,000)/3 = $110,000.

The exact relationship between current and future consumption that each person chooses depends on his individual preferences. Readers familiar with economic theory will know that such choices can be shown by superimposing indifference curves specific to each individual. The preferred combination will be at the intersection of the interest rate line and the individual's indifference curve. In other words, each individual will borrow or lend up to the point where 1 plus the interest rate equals the marginal rate of time preference (ie the slope of the indifference curve). For a more rigorous presentation of graphical analysis of investment decisions and choices between current and future consumption, see the Braley-Myers website at www://mhhe.com/bm/7e.

Some managers, for fear of displeasing any stakeholder group, deny that they are profit or value maximizers. We recall one survey of businessmen in which they were asked to answer whether they were trying to maximize profits. Interviewees indignantly rejected this suggestion, arguing that their responsibilities extended far beyond the narrow and selfish task of making a profit. But when the question was modified slightly and the businessmen were asked whether they could increase their profits by increasing or decreasing the selling price of their products, they replied that none of these changes would lead to a further increase in profits. (See: G. J. Stigler. The Theory of Price. 3rd. ed. New York: Macmillan Company, 1966.)

Under US law, a contract can be valid even if it is not in writing. Of course, it is more reasonable to keep the necessary documentation, but an oral agreement is recognized as valid if it can be proven that the parties have reached complete and unconditional mutual understanding and agreement. For example, in 1984, Getty Oil management verbally agreed to a proposed merger with Pennzoil. Texaco then came out with a better offer and outbid. But Pennzoil sued, alleging that Texaco had breached a valid contract, and won.

For more details on this issue, see: A. Schleifer and L. H. Summers. Breach of Trust in Corporate Takeovers // Corporate Takeovers: Causes and Consequences. Chicago: University of Chicago Press, 1988.

See: Clifford W. Smith, Jr. Economics and Ethics: The Case of Salomon Brothers // Journal of Applied Corporate Finance. 5. 1992. Summer. P. 23-28.

To assess the effectiveness of the project, the company's economists simulate the circulation of invested capital. In order to build models, cash flow and cash flow discounting methodologies are used. The basic parameter of the financial model of a project business plan is NPV, which we will consider in this article. This criterion came into economic analysis in the early nineties and to this day occupies the first position in the comprehensive and comparative assessment of projects.

Basics of project effectiveness assessment

Before we move directly to understanding NPV (net present value), I would like to briefly recall the main points of the evaluation methodology. Its key aspects make it possible to most competently calculate a group of project performance indicators, including NPV. Among the project participants, the main figure interested in evaluation activities is the investor. His economic interest is based on the awareness of the acceptable rate of return that he intends to extract from the actions of placing funds. The investor acts purposefully, refusing to consume available resources, and counts on:

- return of investment;

- compensation for your refusal in future periods;

- better conditions in comparison with possible investment alternatives.

By the rate of return beneficial to the investor, we will understand the minimum acceptable ratio of capital growth in the form of the company’s net profit and the amount of investment in its development. This ratio during the project period should, firstly, compensate for the depreciation of funds due to inflation, possible losses due to the occurrence of risk events, and secondly, provide a premium for abandoning current consumption. The size of this premium corresponds to the entrepreneurial interests of the investor.

The measure of entrepreneurial interest is profit. The best prototype of the profit generation mechanism for the purpose of evaluating an investment project is the flow methodology for reflecting cash flows (CF) from the perspective of income and expense parts. This methodology is called cash flow (CF or cash flow) in Western management practice. In it, income is replaced by the concepts of “receipts”, “inflows”, and expenses - “disposals”, “outflows”. The fundamental concepts of cash flow in relation to an investment project are: cash flow, settlement period and calculation step (interval).

Cash flow for investment purposes shows us the receipts of assets and their disposals arising in connection with project implementation during the entire duration of the billing period. The period of time during which it is necessary to track the cash flows generated by the project and its results in order to evaluate the effectiveness of the investment is called the calculation period. It represents a duration that may extend beyond the time frame of the investment project, including the transition and operational stages, until the end of the equipment life cycle. Planning intervals (steps) are usually calculated in years; in some cases, for small projects, a monthly interval breakdown can be used.

Methods for calculating net income

Of great importance for calculating NPV and other project indicators is how income and expenses are generated in the form of inflows and outflows of business assets. The cash flow methodology can be applied in a generalized form or localized by groups of cash flows (in operational, investment and financial aspects). It is the second form of representation that makes it possible to conveniently calculate net income as the simplest parameter for assessing efficiency. Next, we present to your attention a model of the relationship between the classical grouping of DS flows and grouping according to subject-target criteria.

Scheme of two options for groupings of DS flows with relationships

The nature of the content of the economic effect of investments is expressed in the comparison of the total inflows and outflows of funds at each calculated step of the project task. Net income (CF or BH) is calculated for the corresponding interval value i. Below are the formulas for calculating this indicator. The dynamics of black holes are almost always repeated from project to project. In the first one or two steps, the ND value is negative, because the results of operating activities are not able to cover the size of the investments made. Then the sign changes, and in subsequent periods net income increases.

Formula for calculating net income for period i

The cost of DS changes over time. This is due not only to inflation, but also to the fact that money itself is capable of generating a certain income. Therefore, the cash flow should be brought to the time of the start of the project through the discounting procedure, which uses the net present value method. Thanks to it, ND receives the status of a new indicator called “net present value” or “net present value”. We are no longer interested in step-by-step, but in cumulative discounted cash flow. Its formula is presented below.

Formula for total discounted cash flow

The parameters “discount rate”, “discounted cash flow”, “discount factor” will be discussed in separate material, revealing their financial and economic nature. I will only note that guidelines for the value of r in a project can be the levels of the WACC indicator, the Central Bank refinancing rates, or the rate of return for an investor who is able to secure more profitable alternative investments. The total discounted cash flow can be interpreted and the net present value (NPV) can be calculated from it.

NPV formula

NPV shows us how much money an investor will be able to receive after the size of investments and regular outflows reduced to the initial moment are covered by the same inflows. The “net present value” indicator serves as a successful replica of the Western NPV indicator, which became widespread in Russia during the “boom” of business planning. In our country, this indicator is also called “net present value”. Both English and Russian interpretations of the NPV indicator are equally widespread. The NPV formula is shown below.

NPV formula for the purpose of assessing the effectiveness of a project activity

The net present value presented in the formula is the subject of much debate among practitioners. I do not claim to have the truth, but I believe that domestic methodologists will have to bring some clarity to a number of issues and, perhaps, even correct textbooks. I will express only a couple of comments regarding the main nuances.

- To calculate the “net present value” indicator, one should rely on the classical understanding of net cash flow (NCF) as a combination of operating, investment and financial flows. But investments should be separated from NCF, since common sense discount factors may be different for the two parts of this formula.

- When calculating NPV (NPV), dividends associated with the project must be excluded from the NCF, since they serve as a form of withdrawal of the investor’s final income and should not affect the NPV value of the project.

Net present value, based on these comments, can have several interpretations of the formula, one of which is the option when the discount rate in relation to the size of the investment is based on the WACC or the percentage of inflation. At the same time, the base part of the NCF, adjusted to the initial period at the rate of return, significantly reduces the net present value. The investor’s increased demands on the level of rate r has its consequences, and the net present value decreases or even reaches negative values.

Net present value is not an exclusive indicator of performance and should not be considered in isolation from a group of other criteria. However, NPV represents the main evaluation parameter due to its ability to express the economic impact of a project. Even if the indicator turns out to be slightly above zero, the project can already be considered effective. The formula for calculating NPV in the traditional form of the Western school of management is presented below.

Formula for the net present value of a project

Example of NPV calculation

As we have established, the discount factor carries the investor’s expectations for income from the project. And if during the billing period all project costs are covered by income taking into account discounting, the event is able to satisfy these expectations. The sooner such a moment comes, the better. The higher the net present value, the more effective the project. NPV shows how much additional income an investor can expect. Let's consider a specific example of NPV calculation. Its main initial conditions are:

- the value of the calculation period is 6 years;

- selected planning step – 1 year;

- the moment of starting investment corresponds to the beginning of step “0”;

- the need to obtain borrowed funds is ignored; for simplicity, we assume that investments were made at the expense of the company’s own capital, i.e. CF from financing activities is not taken into account;

- Two options for the discount rate are considered: option A, where r=0.1; option B, where r=0.2.

All initial data on investments and operating CF by project year are given in the table presented.

Example data for calculating the NPV of a project

As a result of filling out the bottom three rows of the table, we are able to calculate the indicators.

- The net income of the project amounted to 3,000 thousand rubles (-300+200+600+1100+1900+2500-3000).

- Net present value for r=0.1, amounting to 687 thousand rubles (-272+165+451+751+1180+1412-3000).

- For the discount rate, r=0.2 amounts to -634 thousand rubles (-250+139+347+530+763+837-3000).

If we compare the three obtained values, the conclusion suggests itself that with a rate of return of 10%, the project can be considered effective, while the investor’s demands for a rate of 20% exclude this event from the zone of his interests. This happens quite often. In recent years, in our economy, the value of the real rate of return has been steadily declining, so relatively few strategic investors come, mainly speculative ones.

In this article, we examined the most popular indicator of assessment, analysis of the economic efficiency of investments and project practice - NPV. When calculating the indicator, the net present value method is used, which allows you to adjust the cash flows generated in the project to changes in the time value of money. The advantage of this criterion is its ability to find an investment effect that is adequate to economic realities, and the disadvantage is its closeness to the investor’s subjective view of the level of expected profitability.

Investing is a direction of financial activity that or loss. It all depends on many factors and risks that such an investment carries. Therefore, there are areas of investment analysis where many indicators are calculated and analyzed, including the present value of the flow.

An investment project is assessed by many indicators, but the main one is the return on investment funds. Also, when investing, each analyst evaluates incoming and outgoing cash flows, which ultimately help evaluate the inflow or outflow at the end of the project.

Cash flow is denoted in theory and practice by CF. This abbreviation is entirely in English. language - cash flow. These are receipts from the project of cash resources, their equivalents, as well as expenses incurred during the duration of the investment. However, not everyone knows that investment activities, already being investment activities, are divided into three main subtypes:

- Flow from investment activities. As a rule, this includes funds received or spent as a result of the acquisition or other intangible assets that are sold or purchased.

- Flow from the financial direction. Includes all flows that are associated with attracting credit funds; with the payment of interest on them, the acquisition and sale of securities, etc.

- Flow from the operating area of activity. Includes income from the provision of services, sales of finished products; expenses for materials, inventories and other components that form.

As a rule, the movement of funds from operating activities is the main one in an enterprise, since it is directly related to its economic activities.

Incoming and outgoing cash flows

Cash flow is the basis for calculating the investment attractiveness of the investment itself, and therefore at each stage of the analysis of this indicator the following components are taken into account:

- How much income was credited to the account of such a project.

- How many expenses were incurred as a result of the sale?

- What is the investment balance: positive or negative.

At the initial stage of investment implementation, flows are predominantly outgoing, and the balance is negative. To calculate the balance, you need to clearly separate what is included in incoming and outgoing flows.

What does the incoming flow of cash resources include:

- products, goods and services

- Obtaining loan funds from the bank and other lenders

- Issue and sale of securities

- Other operating income

- Income from the sale or rental of fixed assets and other intangible assets

- Profit from investments in securities

What does outgoing cash flow include:

- to purchase the necessary materials, raw materials, supplies, semi-finished products, etc.

- Employee wage costs

- Purchase of fixed assets, production facilities

- Funds invested in working capital

- Interest payments on the loan

- Other operating expenses

Based on the results of such indicators, the balance of cash flow of resources can be calculated, which will show the result of investing funds in the business.

Present value: what is it?

Since we are studying such a concept as the present value of the cash flow itself, it is correct to study not only the essence of the cash flow, but also the essence of the concept of “present value”.

Present value allows us to find out the current value of an investment, that is, what we will receive in the future, but subject to the current exchange rate. Present value allows you to determine how much money needs to be invested for a period at interest in order to receive a certain amount of money in the future. In this case, the calculation of present value takes into account compound rather than simple interest.

Why is NPV calculation needed?

If they mean present value, then they mean only the net value. This concept is differently referred to in the world literature as NPV. This completely sounds like Net Present Value. This concept implies the current real amount of monetary resources that are necessary to receive in the near future an amount equal to the income from the sale of this investment.

In simple language: with a deposit interest of 10%, 100 rubles today will be equal to 110 rubles by the end of the year. As a result, such an example of a deposit is equivalent to the profitability of an investment project.

If the investment involves investments not for one year, but for several years, then it is necessary to calculate the present value not at the end of the entire period, but at the end of each reporting year. It is necessary to determine what amount will be returned to the investor at the end of each year in comparison with the investments made in that year.

NPV: is this the same as NPV?

It should also be taken into account that in Russian literature one can often find such an abbreviation as NPV - this is the same thing and is simply deciphered not from English, but from Russian - net present value.

Based on the results of the study, we can conclude that the NPV is the total for all realized cash flows, which is calculated taking into account the current period of time. Present value is always the opposite indicator of future value, which is so often taken as a basis when calculating investment attractiveness.

Algorithm and formula for calculating NPV

NPV = sum of results for each year of investment CF / ((1 + r) to the power of t),

where the designations have the following meaning:

- CF – cash flow balance, calculated as the difference between what the company received and what it spent

- t – number of years for which the calculation is made

- r – investment discount rate

- n – duration of implementation of the investment project itself

When studying cash flows and their present value, it is very important to approach the choice of discount rate directly. When making its choice, it is necessary to take into account not only the features of the theory of the value of money over time, but also take into account the risk of uncertainty. It is better to choose the weighted average as the discount rate invested in the investment project. As a result of this choice, there is a pattern: the greater the risks of uncertainty, the greater the bet itself will be, and vice versa.

NPV of projects: which one to choose

There are two investment projects with investments of 10 thousand rubles. The cash flows for each project by year are known. Project A: 5, 4, 3, 1. Project B has the following cash flows: 1, 3, 4, 6. Discount rate is 10%. Which project is better?

- 5 / (1 + 0.1) to the 1st power = 4545.5

- 4 / (1 + 0.1) to the 2nd power = 3305.8

- 3 / (1 + 0.1) to the 3rd power = 2253.9

- 1 / (1 + 0.1) to the 4th power = 683.0

According to the results of calculating the NPV of the flow for investment project A for 4 years will be: 10788.2 (all NPV for four years are summed up: 4545.5 +…+ 683). If we subtract the initial investment, then NPV = 10788.2 – 10000 = 788.2.

By analogy, the NPV for project B is calculated, where it will be 491.5.

Conclusion: you can invest money in both projects, but it is more profitable to invest in project A.

Analysis of the results obtained

Thus, NPV is a way to study the investment profitability of a project, allowing you to understand today how much money needs to be invested and what the return will be from it. You can also understand how much the project will pay off.

How to analyze results

The implementation of the NPV method is based on the following fundamentals:

- Discounting of cash flows occurs as a whole at the cost of the capital invested. Before carrying out the calculation, it is always necessary to find the size of both incoming and outgoing flows reduced to the current time period, and only after that calculate the NPV.

- All values for discounted cash flows must always be added in order to then evaluate the result obtained.

- The resulting flow is assessed. If the resulting NPV is greater than 0, the investment project can be implemented in reality. If this value is equal to 0, then everything is at the discretion of the investor: the project can be accepted or rejected. This is due to the fact that NPV = 0 indicates that the flows will cover the invested capital and may even provide a small rate of profit, but there will be no further benefits for the investor. The project's share price will not change in the future.

Selection criteria

Based on the results of studying the issue, the criteria for selecting an investment project can be presented as follows:

- If we take into account any investment project, then if the net present value is greater than zero, the project is unconditionally accepted. If such an indicator is negative in the calculation, then the project is clearly rejected. With a value of zero, the investor does not care whether the project is implemented or not.

- If several projects are simultaneously being considered by the investor, then the investment project that has the highest present value is selected from the list, that is, the straightforward selection method is used.

- If there are a lot of projects under consideration, all of which are accepted for implementation by the investor, then if a negative NPV is received, the project must be rejected.

Pros and cons of the method

The main advantage of calculating NPV is that this technique allows the analyst to now estimate the value that will be additionally created in the future, but taking into account modern realities.

This allows the investor to understand the situation and make an informed decision. But we cannot completely say that this method does not have drawbacks; there are some.

Among these controversial issues are the following:

- Incorrect assessment of the discount rate, its sensitivity to changes. Present value calculations are based on the assumption that all investments will be reinvested at the applicable discount rate. But this is absolutely impossible to predict 100%. Interest rates are constantly changing in the financial market, and therefore the one that applies is not a fact that will not change in the future.

- Limitation of project implementation deadlines. Investments can be long-term when it is impossible to estimate cash flows in the future. And the present value may be negative at the time of calculation or at the time of the planned end of the project, and in fact the state of affairs will change a year after the evaluation period.

- Management decisions. The project is assessed for a specific period, but no one appreciates the fact that, given the circumstances and market conditions, top managers can implement creative solutions and change the results of the investment. The manager's reaction can greatly change the magnitude of all flows.

Each investor needs to make the right choice of project, assess its cost, profitability, etc. Flows of cash resources are the fundamental criterion for calculation, and this is an indisputable fact. Present value helps to assess the state of future flows, which is important in the realities of interest capitalization.

Of course, the method is not without its drawbacks, but everyone must make their own decisions about which method to use.

Write your question in the form below

Galtsev Dmitry Alexandrovich

The term “net present value” usually denotes the value of the total discounted values of payment flows, the value of which is given in real time (as of today).

Short abbreviation, NPV. In the specialized literature, other names for this quantity are often used.

For example:

- NPV (net present value). This name is explained by the fact that the flows in question are first discounted and only then added up;

- NPV (net present value). Discounting brings all financial flows to the real (today's) value of money.

International designation – NPV.

Economic meaning of NPV indicator

If we consider the indicator more deeply, we can state that this is the resulting value obtained by taking into account all outgoing and incoming cash receipts of the analyzed investment project, reduced to the time of such analysis.

The resulting value gives the investor an idea of what he can expect when investing (taking into account the repayment of initial costs incurred at the initial stage of project development and periodic outflows during its implementation).

Due to the fact that all cash flows are calculated taking into account risks and time value, the NPV value of an investment project can be characterized as the value added by the project, or as the total profit of the investor.

The main goal of any business is to make a profit.

In order not to invest in risky projects, the investor conducts a preliminary assessment of possible investment options. Moreover, all such proposals at the stage of their preliminary study are evaluated in comparison with the profitability of risk-free investments (bank deposit).

To understand the algorithm for calculating net present value, it should be taken into account that it is based on the methodology of discounting all available cash flows. That is why the decision to invest in a particular project is made after a preliminary calculation of the NPV of the project, within the framework of which:

- all expected inflows and outflows of capital for the accounting period are assessed;

- its value is determined (for the investor this value is considered as a discount rate);

- taking into account the mentioned rate, all incoming and outgoing flows are discounted;

- the results are summarized. The result obtained is the value of the present value of the project.

The resulting number can have the following values.

NPV = 0. This informs the investor that he has a probability of returning the invested funds with a minimal profit.

NPV< 0. Подобные инвестиционные проекты дальнейшему рассмотрению не подлежат.

NPV > 0. The investment should bring profit.

Basic calculation formula:

Symbols used:

- N is the number of periods (months, quarters, years) for which the project being evaluated is calculated;

- t is the time period for which the net present value is considered;

- i is the calculated discount rate for the investment option being evaluated;

- CF t – expected cash flow (net) for a specified time period.

An example of how NPV is calculated (for convenience, we summarize the results in tables and diagrams).

A comparative analysis of two projects with equal starting investments is performed. Let it be 5 million rubles. Both options are characterized by approximately equal risks of uncertainty of available cash flows. For simplicity of calculation, we assume that the cost of raising funds is also the same and equal to 11.5%.

By filling out the form you agree to our privacy policy and consent to the newsletter

The main difference lies in the dynamics of inflows and outflows of funds.

Using the calculation formula given above, we obtain the following discounted flows

The obtained results of the NPV of the project should be interpreted as follows:

- if the investor is offered two independent projects, both should be accepted;

- if they are mutually exclusive, then project “A” has an undeniable advantage, since it has the best NPV.

The value of the discount rate when calculating NPV

When studying net present value, you should definitely pay serious attention to the indicator - the discount rate. It is often referred to differently as the opportunity cost of investment. The indicator used in the calculation formula denotes the minimum return that the investor considers acceptable for risks comparable to those of the project being implemented.

An investor can operate with funds raised from various sources (own or borrowed).

1. In the first case, the discount rate set is a personal assessment of the acceptable risks of the investment project under consideration.

Its assessment can take several approaches. The simplest ones are:

- Selecting a risk-free rate, adjusted taking into account the likelihood of specific risks.

As such, the yield on securities of the state in which the project is being implemented and the rate of return on corporate bonds of companies in the industry are usually considered.

- Necessary and minimum sufficient (from the point of view of a potential investor) profitability (ROE indicator).

In this case, the person making the investment decision determines the discount rate according to one of the possible options:

- funds available on deposit in a specific bank are invested in the project. Therefore, the opportunity cost should not be less than the available bank rate;

- Funds withdrawn from business and temporarily available are invested in the project. If a need arises for them, prompt withdrawal of the entire amount from the project is impossible. A loan will be required. Therefore, the market lending rate is chosen as the current cost of funds;

- The average profitability of the main business is Y%. Accordingly, you are required to receive no less from an investment project.

2. When working with borrowed funds, the rate will be calculated as a derivative of the cost of funds attracted from various sources.

As a rule, the rate set by the investor in such cases exceeds a similar indicator of the cost of borrowed funds.

This not only takes into account changes in the value of funds over time, but also introduces possible risks associated with the uncertainty of cash flows and their volumes.

This is the main reason why the discount rate is considered to be the weighted average cost of capital attracted for subsequent investment (WACC).

It is this indicator that is considered as the required rate of return on funds invested in a specific investment project. The higher the expected risks, the higher the rate.

Calculation methods for determining this parameter are less clear than graphical ones. Especially when you need to compare the attractiveness of two or more projects.

For example, comparing projects “A” and “B” (see graph) the following conclusions can be drawn:

When the rate exceeds 7%, the NPV value of project A is higher than that of B (which warns of a possible error in the choice during arithmetic comparison).

In addition, investment project “B”, indicated on the red curve graph, is subject to more significant changes due to a changing discount rate (this can be explained by different amounts of incoming funds in the same period of time).

It is necessary to take into account the fact of a significant decrease in the value of discount rates over time, which imposes certain time restrictions. They can be calculated in no more than 10 years.

Analysis of the graphs allows us to conclude that a changing discount rate leads to changes in the value of the NPV indicator (and the latter changes nonlinearly).

Therefore, for a more balanced assessment, it is necessary not only to compare the values for different investment projects, but also to take into account changes in the latter at different rates.

By default, when calculating in Excel, the discount rate is assumed to be 10%.

Calculation of NPV using Excel

The program provides the ability to determine the value in question using the “NPV” function.

The operating algorithm is quite simple.

- select “H6” (output cell);

- after pressing fx (button) in the window that opens, first the category – “Financial”, and then the function – “NPV” is selected;

- going to the “Bet” field, select cell “C1”;

- then the range of data used (in this case this is C6:G6) is entered in a special field called “Value 1”. The second field should be left blank “Value 2”. After this, press “OK” (button).

Since the option under consideration does not take into account the initial (starting) investments in the project, you again need to enter “H6”, where you need to add an additional cell “B6” to the formula bar.

Pros and cons of the NPV calculation method

Among the advantages is the use of the so-called discounted cash flow technique. This provides the possibility of adequately assessing such a parameter as the amount of value additionally created as part of the implementation of the investment project.

But a number of serious shortcomings require their mandatory consideration.

These include the following:

- high sensitivity to ongoing changes in discount rates;

- ignoring cash flows, the receipt of which begins after the established deadline for the project.

Join over 3 thousand of our subscribers. Once a month we will send to your email a digest of the best materials published on our website, LinkedIn and Facebook pages.